General

Europe’s Middle-Mile Blind Spot: How AI Orchestration Is Cutting CPG Distribution Costs by Double Digits

Middle-Mile AI Orchestration Defined: A real-time execution layer deployed above ERP systems that dynamically optimizes routing, carrier allocation, load consolidation, and emissions across fragmented distribution networks — processing 180+ constraints simultaneously to deliver 15–20% logistics cost reductions at enterprise scale.

European road freight costs have increased 15–20% since 2021, according to the Transport Intelligence European Road Freight Rate Index. For CPG companies running multi-tier distribution networks, the middle mile — plant to distribution centre, DC to DC, DC to store — is where costs are compounding fastest and visibility is lowest. Last-mile optimization commands attention and investment. Middle-mile operations, often running thousands of routes daily across fragmented carrier networks, remain the quiet margin killer.

The scale of the opportunity is massive and growing. The AI-optimized middle-mile linehaul planning platforms market is valued at USD 680.64 million in 2025 and is predicted to reach USD 2,343.40 million by 2035 at a 13.2% CAGR. Meanwhile, the broader AI orchestration market is projected to increase by USD 12.27 billion at a 21.9% CAGR from 2024 to 2029. These numbers reflect an industry-wide recognition that manual planning and legacy ERP modules cannot keep pace with the constraint density of modern middle-mile logistics.

At the same time, European CPG faces a regulatory compression unique to this region. CSRD mandates Scope 3 emissions reporting from 2024. The EU Clean Vehicle Directive imposes zero-emission fleet quotas from 2025. The EU AI Act requires transparency and auditability for AI in operational decisions from August 2026. All three converge on the same operational layer: middle-mile routing decisions. Every route must now simultaneously optimize for cost, emissions, compliance, and service levels — a constraint-optimization problem that manual dispatch and legacy ERP modules were never designed to solve.

Understanding what is route optimization at a fundamental level is critical — but the middle mile demands optimization at an entirely different scale than last-mile delivery. This is where Locus’s AI-powered orchestration platform transforms operations, and this article explains exactly how.

Key Takeaways

- Europe’s middle mile is the last un-optimized link in CPG distribution. Rising freight costs (15–20% since 2021), 25% empty running rates, and 60% average load factors point to a structural inefficiency problem, not just market conditions.

- ERP-locked routing is the root constraint. 80%+ of European CPG runs SAP, but SAP TM plans routes in batch cycles and cannot optimize dynamically. Manual dispatch fills the gaps across 5,000+ daily routes.

- A regulatory trifecta is compressing timelines. CSRD Scope 3 (mandatory 2024), EU AI Act (August 2026), and the Clean Vehicle Directive (2025) all converge on middle-mile routing decisions — demanding simultaneous optimization for cost, emissions, and compliance.

- Locus’s AI-powered orchestration delivers double-digit cost reductions. Processing 180+ constraints simultaneously — route, carrier, load, emissions, driver hours, delivery windows — has delivered 15–20% logistics cost reductions at enterprise scale within months.

- The market is responding rapidly. The AI-optimized middle-mile planning market is growing at 13.2% CAGR toward USD 2.34 billion by 2035, while AI orchestration broadly is expanding at 21.9% CAGR.

- Deployment sits above your ERP, not in place of it. API-first architecture deploys as an execution layer above SAP/Oracle in weeks to months. No rip-and-replace. Your ERP investment stays intact.

Revolutionize Dispatch Management

Leverage Locus’s advanced dispatch management software to orchestrate middle-mile operations at enterprise scale — above your existing ERP, not in place of it.

Why Europe’s Middle Mile Is Structurally Inefficient

The cost escalation in European CPG middle-mile operations is not a market cycle. It is a structural problem with five compounding root causes.

ERP-Locked Routing

According to Gartner, over 80% of European CPG companies run SAP as their core ERP. Middle-mile routing typically lives in SAP TM or Oracle TM — systems designed for transport planning, not real-time execution. These modules compute routes in batch cycles, often overnight, and produce static plans that dispatchers then execute the following day. They cannot re-optimize dynamically when a carrier cancels, traffic disrupts a corridor, or a promotional surge adds unexpected volume.

The result is predictable: manual dispatching fills the gap. Across European CPG secondary distribution, planners are building and adjusting thousands of routes per day using spreadsheets, phone calls, and accumulated experience. The ERP holds the data. The optimization happens in someone’s head. And upgrading SAP TM itself requires 12–24 month implementation cycles and multi-million-euro investments — a timeline and cost that keeps organizations locked into underperforming systems.

This is precisely the gap that middle-mile AI orchestration fills. Rather than replacing your ERP, Locus’s platform ingests data from SAP TM, applies constraint-based optimization across 180+ variables, and pushes decisions back into the ERP workflow — transforming batch-cycle planning into real-time execution. For enterprises evaluating their options, understanding how to choose the right route planning software that integrates with existing infrastructure is the critical first step.

Also Read: AI Route Optimization to Deal with Europe’s Driver Shortage

Carrier Fragmentation

European CPG secondary distribution relies on a patchwork of owned fleets, contracted hauliers, regional carriers, and spot-market capacity. Most operations have no unified visibility across these pools. Carrier allocation happens through relationships, historical contracts, and manual negotiation — not real-time optimization. When trade-promotion-driven demand spikes 3–5x (common across European CPG categories), static carrier contracts cannot absorb the surge. Spot procurement at premium rates becomes the default — eroding the very margins the promotion was supposed to build.

Empty Running and Load Inefficiency

Eurostat data shows that approximately 25% of truck-kilometres driven in Europe are empty. The European Commission (DG MOVE) reports average load factors of roughly 60% for laden journeys. For CPG secondary distribution — running multi-drop routes with 10–30 stops across mixed temperature zones, each with 30–60-minute retailer delivery windows and penalties for early or late arrival — load optimization is a combinatorial challenge that manual planning consistently underperforms. Every empty kilometre and every underutilized cubic metre of truck capacity is direct margin erosion that compounds across thousands of daily routes.

The Driver Shortage as Cost Multiplier

The IRU Driver Shortage Global Report (2023/2024) documents a shortage of approximately 233,000 truck drivers across Europe, with 21% of positions unfilled. The average driver age is 47; only 6% are under 25. This structural deficit drives persistent wage inflation, which drives transportation cost escalation, which compresses CPG margins year over year. The organizations that can deliver equivalent distribution outcomes with fewer driver-hours — through optimized routing, consolidated loads, and reduced empty running — gain a compounding cost advantage over those still dispatching manually.

The Regulatory Trifecta

European CPG faces a triple regulatory squeeze on middle-mile operations that no other region matches. CSRD requires Scope 3 emissions reporting from 2024 — every middle-mile route contributes to a number that investors, customers, and regulators now track. The EU Clean Vehicle Directive (2025) mandates zero-emission vehicle quotas that affect fleet composition decisions. The EU AI Act (August 2026) requires transparency and auditability for AI systems in operational decision-making. These regulations do not operate in isolation. They converge on the same decision: which truck, which route, which carrier, at what cost, at what emission level, with what audit trail. Manual dispatch cannot manage this compliance complexity at scale.

Organizations pursuing green logistics to build a sustainable supply chain now face a reality where emissions optimization cannot be separated from cost optimization — they must be solved simultaneously within every routing decision.

Why are European CPG middle-mile costs rising?

European CPG middle-mile costs are rising due to five structural factors: ERP-locked routing that cannot optimize dynamically (80%+ of European CPG runs SAP), carrier fragmentation with no unified allocation intelligence, 25% empty running rates and 60% load factors (Eurostat/European Commission), a 233,000-driver shortage inflating wages (IRU, 2024), and a regulatory trifecta — CSRD Scope 3, EU Clean Vehicle Directive, and EU AI Act — all converging on middle-mile routing decisions.

Optimize Your Routes with Locus

Discover how Locus’s AI-powered route optimization processes 180+ constraints simultaneously — cutting middle-mile costs by 15–20% while embedding CSRD compliance into every decision.

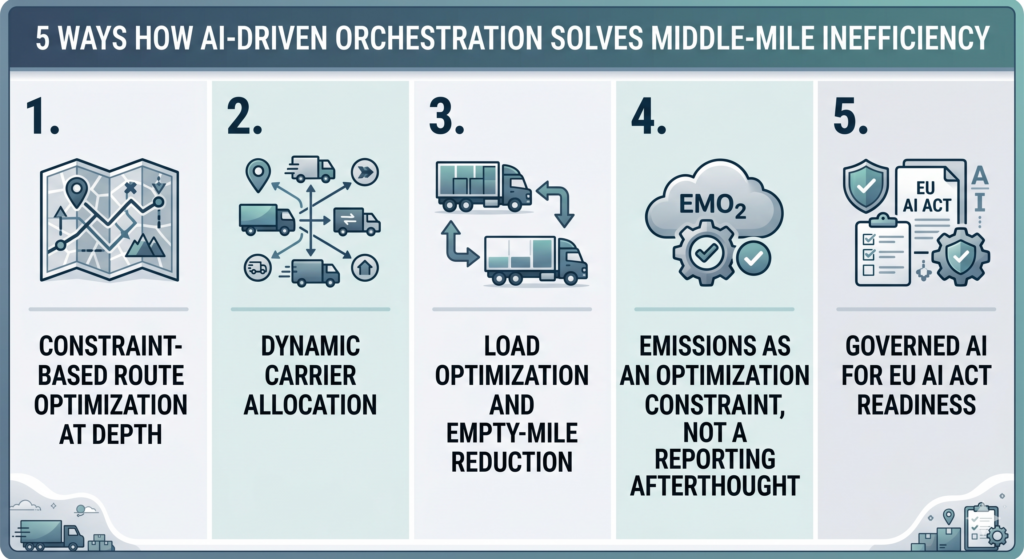

How AI-Driven Orchestration Solves Middle-Mile Inefficiency

The technology required to address Europe’s middle-mile problem is not a better planning tool within your ERP. It is an execution layer that sits above your ERP and orchestrates routing, carrier allocation, load optimization, and compliance simultaneously in real time. Locus’s AI-powered dispatch management platform enables exactly this transformation — and the results at enterprise scale demonstrate why your business needs route optimization at this depth of constraint processing.

Constraint-based route optimization at depth: Advanced AI orchestration engines process 180+ constraints simultaneously per computation — vehicle types and capacities, temperature zones, retailer delivery windows (with early/late penalty structures), European Mobility Package driving-hours compliance, fuel costs, emissions per route segment, carrier availability, cost thresholds, and service-level requirements. This is the computational depth European CPG secondary distribution demands, where each route involves regulatory, operational, and sustainability constraints multiplying against each other. Rule-based modules in ERP systems handle 10–20 of these. The gap between 20 constraints and 180+ is where margin leaks at scale.

Middle-Mile AI Orchestration vs. ERP Planning: Constraint Comparison

| Capability | ERP (SAP TM / Oracle TM) | AI Orchestration (Locus) |

| Constraints processed per computation | 10–20 rule-based | 180+ simultaneous |

| Optimization cycle | Batch (overnight) | Real-time / continuous |

| Carrier allocation | Static contracts, manual spot | Dynamic scoring across 1,000+ carriers |

| Load optimization | Manual / basic rules | Multi-drop, multi-temp, combinatorial |

| Emissions tracking | Separate reporting (post-hoc) | Embedded constraint in route optimization |

| EU AI Act readiness | No governance layer | Built-in explainability, audit trails |

| Deployment timeline | 12–24 months (upgrade) | Weeks to months (API overlay) |

| Forecast accuracy improvement | N/A | Up to 18% enhancement |

Also Read: Carrier Management Software for Multi-Carrier Logistics

Dynamic carrier allocation: Instead of static contracts and manual spot procurement, Locus’s AI orchestration continuously scores carriers across cost, capacity, performance, emissions profile, and regulatory compliance — then autonomously allocates shipments to the optimal carrier mix in real time. When promotional demand surges 3–5x, the system rebalances across owned fleet, contracted hauliers, and spot capacity without dispatcher intervention. With a thousand or more native carrier integrations, the optimization surface is materially larger than what manual allocation or ERP-based carrier selection can access.

Load optimization and empty-mile reduction: AI engines optimize multi-drop load consolidation across temperature zones, weight limits, delivery sequences, and return logistics simultaneously. Recovering even a portion of the 25% empty running and improving the 60% average load factor translates directly to cost reduction and emissions improvement — addressing the P&L and CSRD Scope 3 reporting in the same computation.

Emissions as an optimization constraint, not a reporting afterthought: With CSRD mandating Scope 3 tracking, the ability to calculate and optimize carbon emissions per route — as a constraint within the routing optimization itself, not as a separate sustainability report generated weeks later — becomes a compliance capability. Locus’s platform optimizes for the lowest-emission route configuration that still meets cost and service-level constraints, producing auditable emissions data as a byproduct of every routing decision. Compliance becomes an operational output. According to Technavio, AI orchestration can lower energy consumption by up to 12% through the optimization of AI workflows — a figure that compounds dramatically across thousands of daily middle-mile routes.

Governed AI for EU AI Act readiness: Governance mechanisms — explainability (why this route and carrier were chosen), traceability (complete audit trail from decision to delivery), evaluation (continuous performance measurement against KPIs), autonomy levels (graduated control from human-approved recommendations to full autonomous dispatch), and human-in-the-loop escalation — prepare organizations for EU AI Act compliance before the August 2026 deadline. Platforms with built-in governance, like Locus, are in a fundamentally different regulatory position than black-box optimizers that will require retrofitting.

Middle-Mile AI Orchestration vs. Autonomous Trucking

A common question is how AI orchestration compares to autonomous trucking solutions like Gatik’s middle-mile AV operations. The distinction is fundamental: autonomous trucking optimizes individual vehicle operation on repeatable, fixed routes using HD maps and sensor fusion. AI orchestration optimizes the entire network — which trucks, which routes, which carriers, which loads, at what emissions profile — across hundreds of locations and thousands of daily routes. Autonomous trucking solves a hardware problem on controlled routes. AI orchestration solves a network-wide decision problem across fragmented carrier ecosystems. They are complementary, not competitive — but orchestration delivers ROI today without waiting for regulatory approval of autonomous vehicles.

How does AI reduce middle-mile logistics costs in European CPG?

Locus’s AI-powered orchestration platform reduces middle-mile costs through four mechanisms: constraint-based route optimization processing 180+ variables simultaneously (vs. 10–20 in ERP modules), dynamic carrier allocation across fragmented fleet networks, load consolidation that reduces 25% empty running and improves 60% load factors, and emissions-per-route optimization that makes CSRD Scope 3 compliance an operational byproduct. Enterprise implementations deliver 15–20% logistics cost reductions within months.

The Business Impact: What Double-Digit Reduction Looks Like

Logistics cost reduction. Enterprise-scale AI route and carrier orchestration has demonstrated 15–20% logistics cost reductions in CPG distribution operations within months of deployment. This is achieved through the compounding effect of route optimization, carrier allocation improvement, load consolidation, and empty-mile reduction — not any single lever. For a European CPG operation spending €50–100 million annually on secondary distribution, a 15% reduction translates to €7.5–15 million recovered annually.

Operational downtime reduction. Beyond direct cost savings, implementing AI orchestration can lead to a 30% reduction in operational downtime — eliminating the cascading delays that occur when manual dispatch fails to adapt to carrier cancellations, traffic disruptions, or volume surges. For CPG distribution networks where every hour of delay compounds across downstream retail delivery windows, this operational resilience translates directly to service-level improvements and reduced penalty costs.

Forecast accuracy gains. AI orchestration doesn’t just optimize today’s routes — it learns from every execution cycle. AI orchestration can deliver an 18% enhancement in forecast accuracy, enabling proactive capacity planning that reduces both the cost of over-provisioning and the margin erosion of emergency spot procurement during demand surges.

Driver-hour efficiency. Optimized routing reduces total driver-hours required for equivalent delivery volume. In a market where 21% of driver positions are unfilled (IRU), reducing the driver-hours needed per route is a direct structural response to the labour shortage. This is not about replacing drivers — it is about ensuring every driver-hour produces maximum distribution output through routes that are optimized for distance, time, load, and delivery sequence simultaneously.

European CPG operation spending €50–100 million annually on secondary distribution, a 15% reduction translates to €7.5–15 million recovered annually.

Compliance as operational capability. CSRD Scope 3 data generated as a byproduct of every optimized route. EU AI Act auditability built into the governance framework. Fleet emission profiles aligned with Clean Vehicle Directive targets. When compliance is an output of your routing optimization rather than a separate reporting workstream, the regulatory trifecta becomes a capability differentiator — not just a cost of doing business.

Deployment without disruption. The critical deployment reality for European CPG: any solution must work above SAP or Oracle via API-first architecture — not replace it. The organizations achieving double-digit cost reductions are deploying Locus’s AI orchestration as an execution layer above their existing ERP in weeks to months, preserving their multi-million-euro SAP investment while adding the real-time optimization capability SAP TM lacks. For operations looking to automate logistics operations without infrastructure disruption, this API-first approach eliminates the 12–24 month ERP upgrade cycle entirely. The execution layer handles what the ERP cannot: dynamic, constraint-governed routing decisions at the speed European CPG distribution demands.

What ROI does AI orchestration deliver for European CPG distribution?

Locus’s AI-driven middle-mile orchestration delivers 15–20% logistics cost reductions at enterprise scale within months. For a CPG operation spending €50–100M on secondary distribution, this translates to €7.5–15M annual savings. Additional ROI includes 30% operational downtime reduction, 18% forecast accuracy improvement, driver-hour efficiency gains (critical with 21% of positions unfilled), CSRD Scope 3 compliance as an operational byproduct, and EU AI Act audit readiness through built-in governance mechanisms.

Benefits of Middle-Mile AI Orchestration for European CPG

The compounding benefits of middle-mile AI orchestration extend beyond isolated cost savings. Here is what enterprise CPG distributors gain:

- 15–20% logistics cost reduction through simultaneous optimization of routes, carriers, loads, and emissions — not through any single lever, but through the multiplicative effect of solving all constraints together.

- 30% reduction in operational downtime by dynamically adapting to carrier cancellations, traffic disruptions, and volume surges in real time rather than relying on next-day batch replanning.

- 25% empty running recovery by optimizing backhaul logistics, load consolidation, and return route planning across multi-drop, multi-temperature-zone networks.

- 18% improvement in forecast accuracy through continuous learning from every executed route, enabling proactive capacity planning and reducing emergency spot procurement costs.

- 12% energy consumption reduction via AI workflow optimization that compounds across thousands of daily routes, directly improving both P&L and CSRD Scope 3 metrics.

- EU AI Act compliance by design with built-in explainability, full audit trails, and human-in-the-loop escalation — eliminating the risk and cost of retrofitting black-box systems before August 2026.

- Driver-hour efficiency gains that structurally address the 233,000-driver shortage across Europe by ensuring maximum distribution output per driver-hour through optimized sequencing and reduced empty running.

- Deployment in weeks, not years via API-first architecture that sits above SAP/Oracle, preserving existing ERP investments while adding the dynamic execution capability legacy systems lack.

These benefits do not operate independently — they compound. A route that reduces empty running simultaneously lowers fuel costs, cuts emissions, reduces driver-hours, and improves carrier utilisation. This is the fundamental advantage of constraint-based AI orchestration over siloed optimisation tools.

Why Choose Locus for Middle-Mile AI Orchestration

Locus’s AI-powered orchestration platform is purpose-built for the constraint density and regulatory complexity of European CPG distribution. Here is what differentiates Locus:

180+ constraint processing depth. Locus’s engine processes vehicle capacities, temperature zones, retailer delivery windows with penalty structures, European Mobility Package driving-hours compliance, fuel costs, emissions per route segment, carrier performance scores, cost thresholds, and service-level requirements — simultaneously, in real time. ERP modules handle 10–20 of these. Locus handles 180+. The 9x difference in constraint depth is where double-digit cost reductions originate.

1,000+ native carrier integrations. Locus delivers agentic transportation management from order intake to freight settlement, with dynamic carrier scoring that continuously evaluates cost, capacity, performance, emissions profile, and regulatory compliance across the full carrier ecosystem — owned fleet, contracted hauliers, and spot market. When demand surges 3–5x, the platform autonomously rebalances allocation without dispatcher intervention.

Built-in EU AI Act governance. Explainability, traceability, continuous KPI evaluation, graduated autonomy levels, and human-in-the-loop escalation are architectural features — not retrofit additions. Locus provides complete audit trails from routing decision to delivery outcome, positioning enterprises for EU AI Act compliance as an operational capability rather than a compliance project.

CSRD Scope 3 compliance as operational byproduct. Every route optimized through Locus produces auditable carbon emissions data. Emissions are a constraint within the optimization itself — the platform finds the lowest-emission configuration that still meets cost and service targets. Compliance reporting becomes a data export, not a quarterly scramble.

API-first ERP integration. Locus deploys as an execution layer above SAP and Oracle in weeks to months, not years. No rip-and-replace. Your multi-million-euro ERP investment stays intact. Locus adds the real-time, constraint-governed routing execution that SAP TM and Oracle TM lack.

Proven enterprise scale. Locus operates across CPG distribution networks spanning hundreds of locations, processing thousands of routes daily. The platform has demonstrated 15–20% logistics cost reductions within months of deployment — documented, measurable, and repeatable.

For enterprises evaluating route optimization software at this scale, Locus represents the difference between incremental improvement and structural transformation.

Expert Supply Chain Consulting

Partner with Locus for tailored supply chain solutions — from middle-mile orchestration strategy to full deployment above your existing ERP infrastructure.

The Middle Mile Cannot Wait

Europe’s middle mile is the last un-optimized link in CPG distribution — trapped between ERPs that plan but cannot execute, carrier networks with no unified intelligence, a structural driver shortage that inflates costs year over year, and a regulatory environment that now demands simultaneous optimization for cost, emissions, and compliance on every route.

The technology to solve this exists and operates at enterprise scale: Locus’s AI-driven orchestration platform processes 180+ constraints, allocates carriers dynamically across 1,000+ integrations, optimizes loads and emissions per route, and deploys above your existing ERP infrastructure in months without disruption. Enterprise implementations have proven double-digit cost reductions across CPG distribution networks spanning hundreds of locations — with 30% operational downtime reduction and 18% forecast accuracy improvement as additional documented outcomes.

The regulatory deadlines are not moving. CSRD is live. The Clean Vehicle Directive is in effect. The EU AI Act arrives August 2026. The organizations that deploy governed, auditable AI orchestration now will meet each deadline as an operational capability. Those that wait will face the same cost pressures with the added burden of compliance scrambles.

With the AI-optimized middle-mile planning market projected to reach USD 2.34 billion by 2035, the direction is clear. The question is not whether European CPG will adopt middle-mile AI orchestration — it is whether your organization will capture the 15–20% cost advantage now or concede it to competitors who move first.

The middle mile has been a blind spot long enough.

Frequently Asked Questions (FAQs)

What is middle-mile AI orchestration?

Middle-mile AI orchestration is a real-time execution layer deployed above existing ERP systems that dynamically optimizes routing, carrier allocation, load consolidation, and emissions across fragmented distribution networks. Locus’s AI-powered orchestration platform processes 180+ constraints simultaneously — including delivery windows, driver hours, temperature zones, and CSRD Scope 3 emissions — delivering 15–20% cost reductions in European CPG distribution. Unlike ERP’s 10–20 rule-based constraints, it enables autonomous decisions across fragmented fleets at enterprise scale.

Why is the middle mile the most expensive part of CPG distribution in Europe?

The middle mile — plant to DC, DC to DC, DC to store — accounts for 30–40% of total CPG logistics costs and is rising at 15–20% year-on-year (Transport Intelligence). Five structural factors drive this: ERP-locked routing that cannot optimize dynamically (80%+ of European CPG runs SAP), carrier fragmentation with no unified allocation, 25% empty running rates (Eurostat), a 233,000-driver shortage inflating wages (IRU, 2024), and converging EU regulations (CSRD, Clean Vehicle Directive, EU AI Act) adding compliance complexity to every routing decision. The AI-optimized middle-mile planning market reaching USD 680.64 million in 2025 reflects the scale of enterprise investment now flowing toward solving this structural problem.

How does AI orchestration reduce middle-mile logistics costs?

Locus’s AI-powered orchestration platform reduces middle-mile costs through four compounding mechanisms: constraint-based route optimization processing 180+ variables simultaneously (vs. 10–20 in ERP modules), dynamic carrier allocation that rebalances across owned fleet and contracted/spot capacity in real time, load consolidation that reduces empty running and improves the 60% average load factor, and emissions-per-route optimization that embeds CSRD Scope 3 compliance into the routing computation. Enterprise implementations deliver 15–20% cost reductions within months, with additional gains from 30% operational downtime reduction and 18% forecast accuracy improvement.

Can AI routing platforms integrate with SAP TM without replacing it?

Yes. Locus’s AI orchestration platform is built with API-first architecture specifically to deploy above existing ERP systems like SAP and Oracle. The platform functions as an execution layer — ingesting data from SAP TM, optimizing routing, carrier allocation, and load configuration in real time, and pushing decisions back into the ERP workflow. This deploys in weeks to months, preserving the existing SAP investment while adding the dynamic optimization capability SAP TM lacks. For enterprises assessing this integration path, evaluating route optimization software designed for API-first ERP overlay is the critical selection criterion.

How does the European driver shortage affect middle-mile costs?

The IRU reports a shortage of approximately 233,000 truck drivers across Europe with 21% of positions unfilled. The average driver age is 47 with only 6% under 25, indicating the shortage will deepen. This drives persistent wage inflation that directly increases transportation costs. AI-driven route optimization addresses this by reducing total driver-hours required per delivery volume through optimized routing, load consolidation, and reduced empty running — making every driver-hour maximally productive rather than replacing drivers.

How does CSRD Scope 3 compliance relate to middle-mile routing?

CSRD mandates Scope 3 emissions reporting from 2024 for large European companies. Middle-mile distribution is a significant Scope 3 contributor for CPG brands. Locus’s AI orchestration platform calculates emissions per route as a constraint within the optimization — rather than as a separate reporting exercise — producing auditable emissions data as a byproduct of every routing decision. This makes Scope 3 compliance an operational capability embedded in daily routing, not a quarterly reporting scramble. Additionally, AI orchestration can lower energy consumption by up to 12%, compounding the emissions reduction across thousands of daily routes.

What does the EU AI Act mean for logistics AI platforms?

The EU AI Act, taking full effect August 2026, mandates transparency and auditability for AI systems used in operational decision-making. For logistics, this means AI routing platforms must demonstrate explainability (why decisions were made), traceability (audit trails from decision to delivery), and human-in-the-loop capabilities. Locus’s platform includes built-in governance mechanisms — explainability, traceability, continuous KPI evaluation, graduated autonomy levels, and human-in-the-loop escalation — positioning enterprises for compliance as an architectural feature rather than a retrofit project. Platforms without these governance capabilities will require significant re-engineering before the deadline, creating both cost and operational risk.

How does middle-mile AI orchestration differ from autonomous trucking?

Middle-mile AI orchestration and autonomous trucking solve fundamentally different problems. Autonomous trucking (e.g., Gatik) optimises individual vehicle operation on fixed, repeatable routes using HD maps and sensor fusion within controlled operational design domains. AI orchestration optimises the entire distribution network — which vehicles, which routes, which carriers, which loads, at what emissions profile — across hundreds of locations and fragmented carrier ecosystems processing 180+ constraints simultaneously. Orchestration delivers enterprise-wide ROI today through Locus’s API-first platform, while autonomous trucking remains limited to specific corridors and regulatory approval timelines. The two are complementary, but orchestration addresses the immediate structural cost problem European CPG faces now.

What is the market outlook for middle-mile AI orchestration?

The AI-optimized middle-mile linehaul planning platforms market is valued at USD 680.64 million in 2025 and projected to reach USD 2,343.40 million by 2035 at a 13.2% CAGR. The broader AI orchestration market is expected to grow by USD 12.27 billion at a 21.9% CAGR from 2024 to 2029. North America currently leads adoption, but Europe’s unique regulatory drivers — CSRD, Clean Vehicle Directive, and the EU AI Act — are accelerating demand for governed, compliance-embedded orchestration platforms like Locus at a rate that may close the regional gap within the forecast period.

What key constraints does middle-mile AI route optimization process?

Locus’s AI orchestration engine processes 180+ constraints per computation, including: vehicle types and capacities, temperature zones, retailer delivery windows with early/late penalty structures, European Mobility Package driving-hours compliance, fuel costs, emissions per route segment, carrier availability and performance scores, cost thresholds, backhaul logistics, and service-level requirements. This constraint depth is the core differentiator — ERP modules handle 10–20 constraints via rule-based logic, while Locus’s 180+ constraint processing captures the combinatorial complexity that drives 25% empty running and 60% load factors down to significantly more efficient levels.

General

Reducing Failed Deliveries in the Philippines: A Guide for Enterprise Urban Last-Mile Logistics

Apr 17, 2026

Failed delivery rates in SEA megacities reach 30–40%+. Learn how AI geocoding and constraint-based dynamic routing solve the address quality, traffic, and urban complexity challenges unique to the region.

Read more

General

How to reduce failed delivery attempts across the Middle East & Africa

Apr 20, 2026

Failed deliveries cost MEA enterprises millions. Learn how AI dispatch orchestration improves first-attempt delivery success across MEA's carrier networks.

Read moreInsights Worth Your Time

Europe’s Middle-Mile Blind Spot: How AI Orchestration Is Cutting CPG Distribution Costs by Double Digits